As per the recent news, IndusInd Bank in the Maharashtra state of India launched a pilot program encouraging farmers to exchange carbon credits for Central Bank Digital Currency (CBDC) using digital wallets. This project aims to increase digital currency adoption in the agricultural sectors and their transactions.

The above-referenced news illustrates the adoption of the Central Bank Digital Currencies (CBDCs) across multiple sectors. Let us first look at the definition of CBDCs. Central Bank Digital Currencies (CBDCs) are digitalized formats of the fiat currency of any country, issued by their central banks. These digital currencies aim to complement traditional currencies by incorporating multiple benefits, instead of replacing them.

Now, the question arises- what are tokenized CBDCs? Tokenized CBDCs are a form of digital currencies that are issued by the central banks of the countries and are represented in the form of tokens on the blockchain technology. CBDC Tokenization can improve transactions and facilitate programmable features. Let us learn more about CBDC tokenization, its economic benefits, the advantages of tokenizing CBDCs for financial institutions, and use cases for tokenized CBDCs.

Key Takeaways:

- A brief overview of Central Bank Digital Currencies (CBDCs) and tokenization in CBDCs.

- Tokenizing CBDCs enhances security, efficiency, and programmability.

- The perks of tokenizing CBDCs for financial inclusion include financial inclusion, enhanced security, reduced cash handling risks, and cost reduction.

- The role of blockchain technology in CBDC tokenization awards immutability, traceability, security, and transparency.

- Use cases of tokenized CBDCs include cross-border payments, micropayments, government programs, and retail payments.

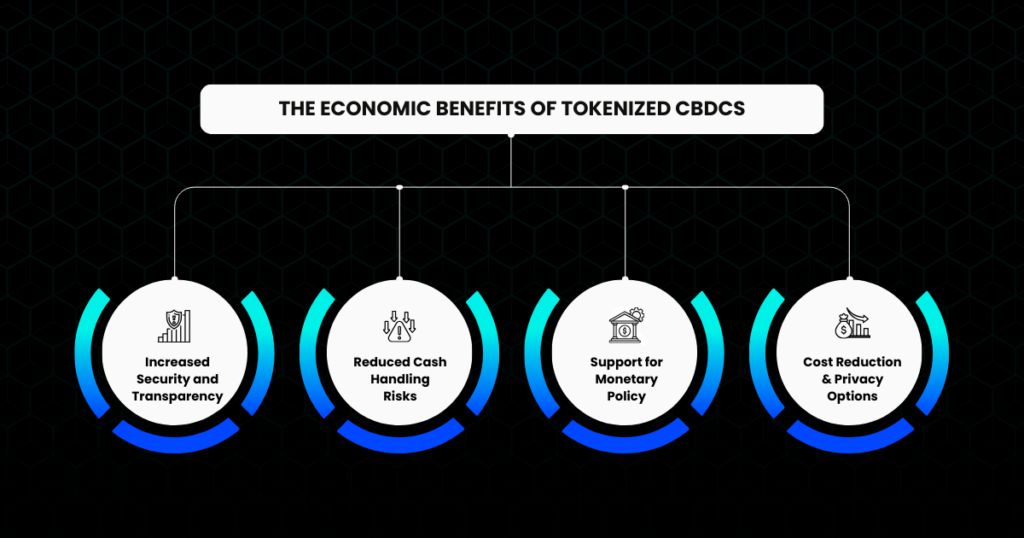

How CBDC Tokenization Adds Value?

The benefits of tokenizing Central Bank Digital Currencies (CBDCs) include increased security, transparency, and reliability due to blockchain technology. This step can reduce the cash handling risks by providing digital alternatives to the cash. It also presents a more financially inclusive domain, allowing users from multiple backgrounds to participate. Moreover, by utilizing smart contracts, tokenized CBDCs reduce costs by automating the process and reducing the intermediaries involved in the operations and transactions.

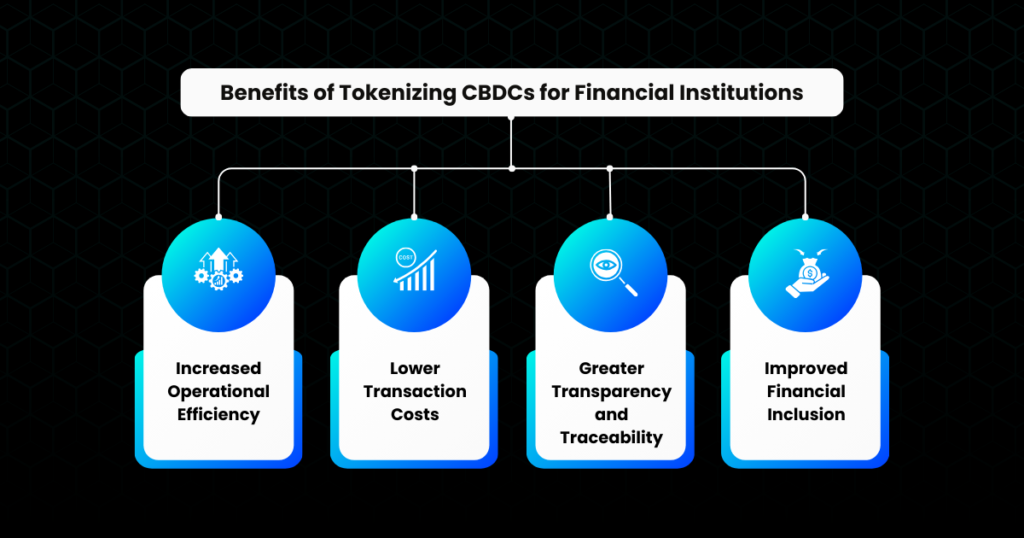

The Benefits of CBDC Tokenization for Financial Institutions

The role of tokenization in CBDC is not limited to programmability but also enhances security, transparency, and immutable records of transactions for these currencies, improving the functioning of financial institutions. The following are the benefits of CBDC tokenization for financial institutions:

Increased Operational Efficiency

Tokenization of Central Bank Digital Currencies (CBDCs) helps in making operational efficiency better by streamlining transactions. Further, tokenization permits instant settlement which reduces time and complexity, especially in the case of interbank transactions. This approach minimizes delays that are prevalent in traditional systems and optimizes overall operational efficiency.

Lower Transaction Costs

Financial inclusion with CBDC Tokenization is another significant aspect due to significantly lower transaction costs for financial institutions. Further, digital currency tokenization omits the need to rely on intermediaries such as traditional banking systems, trustees, and other financial institutions. This reduces transactional costs, which is an advantageous position for not just consumers but also for institutions.

Greater Transparency and Traceability

Tokenization in CBDC allows increased transparency and traceability during the process of transaction. Tokenization leverages blockchain technology that provides an immutable record of transactions for tracking and verifying the movements of funds securely. These build trust among the users and institutions by providing verifiable records of all transactions.

Improved Financial Inclusion

Tokenizing CBDCs encourages financial inclusion by providing access to digital currencies for all the people, equally. Further, it lowers barriers to entry and the ability to transact without traditional banking infrastructure. Tokenization allows individuals from underserved regions to participate in the digital economy.

Use Cases for Tokenized CBDCs

Tokenized Central Bank Digital Currencies (CBDCs) are an innovative technology that presents multiple use cases for reforming financial institutions, transactions, and economic efficiency. These tokenized currencies allow several advantages, some of the most prominent ones are:

Cross-Border Payments

Tokenized Central Bank Digital Currencies (CBDCs) help streamline cross-border transactions by minimizing transactional costs and processing times. Further, it utilized blockchain technology that allows real-time settlement between different currencies, minimizing the need for intermediaries. This framework smoothens financial operations and makes international trade transparent and efficient.

Micropayments

Tokenization in CBDCs allows efficient micropayments by granting users, consumers, and institutions minimal charges. This step is beneficial for consumers, especially digital content creators, app developers, and service providers as they heavily rely on microtransactions for the generation of revenue. Moreover, the cost reduction also aids small business models and improves user experience.

Government Programs

The governmental programs can also be augmented by leveraging tokenized CBDC as it can improve their deliverables by permitting direct distributions of benefits, services, and subsidiaries. Further, its real-time tracking along with transparency and security can ensure better fund allocation reaching the intended recipients. Governments can systemize administrative costs and minimize fraud risks associated with traditional disbursement methods.

Retail Payments

Tokenizing CBDCs can potentially modify the retail payment system through its secure and transparent eco-system. In this structure, consumers and users can utilize digital wallets to purchase products or services. This reduces transactional costs, and delays, with security features, encouraging participation among the users.

As tokenization in real-world assets is gaining momentum in the market; several platforms allow their trading and investment. One such platform is STOEX.

STOEX is backed by KALP Distributed Ledger Technology (DLT) and strictly adhered to regulatory compliance, ensuring transparency and liquidity. With its structured approach, stringent security, and commitment to compliance, the platform offers an appealing option for diversified and efficient investing. Its regulation, security measures, focus on usability and customer-centric approach make it stand out as an accessible way of trading tokenized real-world assets.

Additionally, STOEX’s vision is to build a ground with reduced entry barriers and encourage a safe ecosystem for every individual interested in investing in the market. It pulls the strings of financial democratization by bridging the gap between investors and high-worth tokenized RWAs.

Final Insights

Tokenization in Central Bank Digital Currencies (CBDCs) can potentially change the financial domain by reforming traditional currencies with their multiple positive aspects. By utilizing blockchain technology, tokenized CBDCs provide several benefits such as security, transparency, immutability, traceability, and efficiency for both financial institutions and users. Further, they grant advantages such as increased operational efficiency, lower transaction costs, greater transparency, and traceability.

As these concepts are still evolving, various platforms are adding to the layer of opportunities and options within these domains. One such option is STOEX, which allows investors to access the marketplace and trade effortlessly.

For more information and queries, please visit STOEX.

FAQs

What is CBDC tokenization?

CBDC tokenization refers to the process of converting a central bank-issued digital currency (CBDC) into digital tokens.

How does tokenization improve the efficiency of CBDCs?

Tokenization allows CBDCs to be transferred instantly with lower transaction fees, enhanced security, and increased programmability, improving efficiency.

What are the main advantages of CBDC tokenization over traditional currencies?

The main advantages of CBDC tokenization over traditional currencies are faster transactions, greater transparency, better traceability, and reduced fraud risk.

Will CBDC tokenization replace traditional currencies?

While CBDC tokenization might revolutionize how digital transactions are conducted, it is unlikely to fully replace traditional fiat currencies.

What are the key challenges associated with CBDC tokenization?

The key challenges include ensuring privacy and security, overcoming regulatory hurdles, and achieving interoperability between countries.